Here is the report by the U.S. Financial Crisis Inquiry Commission (pdf)

When the Financial Crisis Inquiry Commission released their final forensic report on the causes of the 2008 financial collapse on Wall Street – the worst collapse since the 1929-1932 collapse – it pointed to hidden leverage in off-balance sheet entities at the megabanks on Wall Street as a key driver of the crisis. It wrote:

“From 2000 to 2007, large banks and thrifts generally had $16 to $22 in assets for each dollar of capital, for leverage ratios between 16:1 and 22:1. For some banks, leverage remained roughly constant. JP Morgan’s reported leverage was between 20:1 and 22:1. Wells Fargo’s generally ranged between 16:1 and 17:1. Other banks upped their leverage. Bank of America’s rose from 18:1 in 2000 to 27:1 in 2007. Citigroup’s increased from 18:1 to 22:1, then shot up to 32:1 by the end of 2007, when Citi brought off-balance sheet assets onto the balance sheet. More than other banks, Citigroup held assets off of its balance sheet, in part to hold down capital requirements. In 2007, even after bringing $80 billion worth of assets on balance sheet, substantial assets remained off. If those had been included, leverage in 2007 would have been 48:1, or about 53% higher. In comparison, at Wells Fargo and Bank of America, including off-balance-sheet assets would have raised the 2007 leverage ratios 17% and 28%, respectively.”

Citigroup, of course, blew itself up in 2008 and received the largest bailouts in global banking history. By March of 2009, its stock was trading at 99 cents.

The crash of 1929-1932 had two key similarities to today’s banking structure: so-called universal banks that took deposits as well as operated giant trading casinos that took huge risks by speculating in stocks and manipulating markets; and the lack of competent regulation.

The Banking Act of 1933, known also as the Glass-Steagall Act, effectively dealt with that crisis for the next 66 years by barring deposit-taking banks from merging with Wall Street trading houses. The Bill Clinton administration repealed that legislation in 1999 at the urging of Sandy Weill, John Reed (and their sycophants in his administration) in order for the two men to recreate the disastrous 1929 universal bank model via the creation of Citigroup. The other big players on Wall Street followed in lockstep in short order.

In January of this year, Anat Admati, Professor of Finance and Economics at Stanford Graduate School of Business, and German economist Martin Hellwig, released an updated and expanded version of their 2013 book The Bankers’ New Clothes: What’s Wrong with Banking and What to Do about It. In it, the authors write:

"Some of the risks that make JPMorgan Chase dangerous cannot actually be seen by looking at its balance sheet because the positions that give rise to them are not included there. These are risks from business units that JPMorgan Chase might own in part or that it sponsors, and to which it has provided guarantees to serve as a backstop if they should have funding problems. These units might be full-flown subsidiaries, or they might be mere ‘letterhead firms,’ vehicles without any drivers, that are established for legal or tax reasons only. The bank’s commitments to these units amount to almost a trillion dollars, but these potential liabilities of the bank are left off the bank’s balance sheet. Yet they are quite relevant to the financial health of JPMorgan Chase.”

JPMorgan Chase explains why it doesn’t consolidate its tax credit vehicles on its balance sheet as follows in its most recent annual report:

“The Firm holds investments in unconsolidated tax credit vehicles, which are limited partnerships and similar entities that own and operate affordable housing, energy, and other projects. These entities are primarily considered VIEs [Variable Interest Entities]. A third party is typically the general partner or managing member and has control over the significant activities of the tax credit vehicles, and accordingly the Firm does not consolidate tax credit vehicles….”

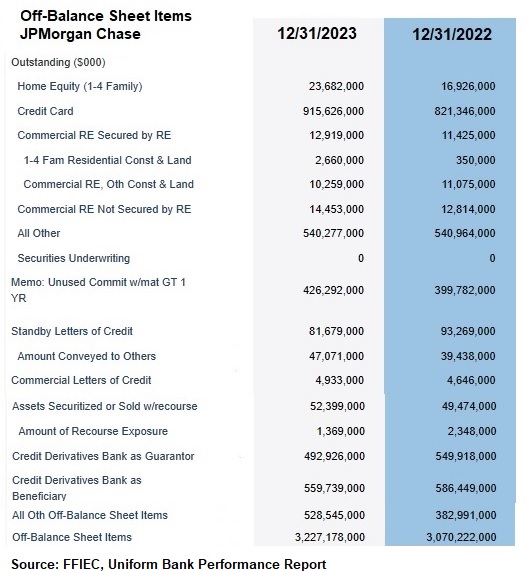

But that’s just the tip of the iceberg. According to financial data at the Federal Financial Institutions Examination Council (FFIEC), as of December 31, 2023, JPMorgan Chase held $3.227 trillion off-balance sheet, of which $528.5 billion is undefined and marked as “other.” To put that in perspective, $528.5 billion is the size of the assets of the seventh largest bank in the United States and yet the public has no idea what the $528.5 billion off-balance sheet at JPMorgan Chase is made up of or what kind of risks it presents.

In JPMorgan Chase’s 10-K public filing with the Securities and Exchange Commission for the period ending December 31, 2023, it reported total assets on its balance sheet of $3.875 trillion. (See page 46 at this link.) That’s versus the FFIEC data showing it has another $3.227 trillion off-balance sheet. Now ask yourself this: have you ever read in any mainstream media news outlet that the U.S. is harboring a $7.1 trillion bank that has admitted to five criminal felony counts since 2014?

JPMorgan Chase’s off-balance sheet hubris goes a long way in explaining why the bank’s federal regulators are demanding that it increase its capital by 25 percent. The bank’s Chairman and CEO, Jamie Dimon, is huffing and puffing against a capital increase and holding all of those private meetings with bigwigs in Washington.

Raising additional concerns, for the first time ever Jamie Dimon dumped a large amount of his own stock in JPMorgan Chase this year, selling $150 million in February and another $32.8 million in April. If the bank is forced by its regulators to announce a big equity capital raise via a secondary offering of common stock, that could cause a plunge in its share price – raising more questions about the timing of Dimon’s unprecedented stock sales while sitting on inside information gleaned from what his bank regulators are telling him about its demands for an increase in capital.

JPMorgan Chase, of course, is not the only Wall Street megabank showing giant sums off-balance sheet. As of December 31, 2023 Bank of America shows $1.6 trillion off-balance sheet; and Citigroup’s Citibank, the “universal” bank that blew itself up in 2008, shows a mind-boggling $2.6 trillion off-balance sheet versus $1.7 trillion on its balance sheet. That data also comes courtesy of FFIEC.

JP Morgan Chase’s off-balance sheet items can be seen here (jpg)

{kind=link}

I would. These banks are and have always been highly corrupt, which will happen when you aren’t properly regulated. There’s just no reason not to gamble with people’s money (off the books of course) since Uncle Sam will pay you back the losses out of public money.

Imagine you’re planning a big party and you’ve set a budget for how much you can spend on food, decorations, and entertainment. To stick to your budget, you decide not to include the cost of some items, like extra snacks and drinks, in your official party budget. Instead, you plan to buy these items using separate money that you haven’t counted in your main budget.

In this analogy, your official party budget is like a bank’s balance sheet, which shows all the assets and liabilities they officially recognize. The extra snacks and drinks are like off-balance sheet assets—they’re costs and commitments that exist but aren’t included in the main budget (or balance sheet) that everyone sees. Just like how not accounting for these extra items might make your party budget look more manageable, keeping assets off the balance sheet can make a bank’s financial health appear better than it actually is, potentially hiding risks or liabilities.